FIFO (First In, First Out) and LIFO (Last In, First Out) are the two most widely used inventory valuation methods in maintenance and manufacturing operations. FIFO assumes the oldest stock is consumed first, while LIFO assumes the newest stock is used first. The method you choose directly affects your cost of goods sold, tax liability, and the accuracy of your inventory records — which is why getting it right matters.

For maintenance teams managing spare parts, consumables, and MRO inventory, the difference between FIFO and LIFO is not just an accounting preference. It shapes how you report costs, plan budgets, and respond to price changes. According to a Deloitte analysis of IAS 2 inventory standards, LIFO is actually prohibited under IFRS — meaning global operations must understand which method applies to them before making a choice.

This guide breaks down both methods with clear examples, walks through the real tax and operational implications, and helps you decide which approach fits your facility's needs — including how a modern CMMS can automate the calculation for you.

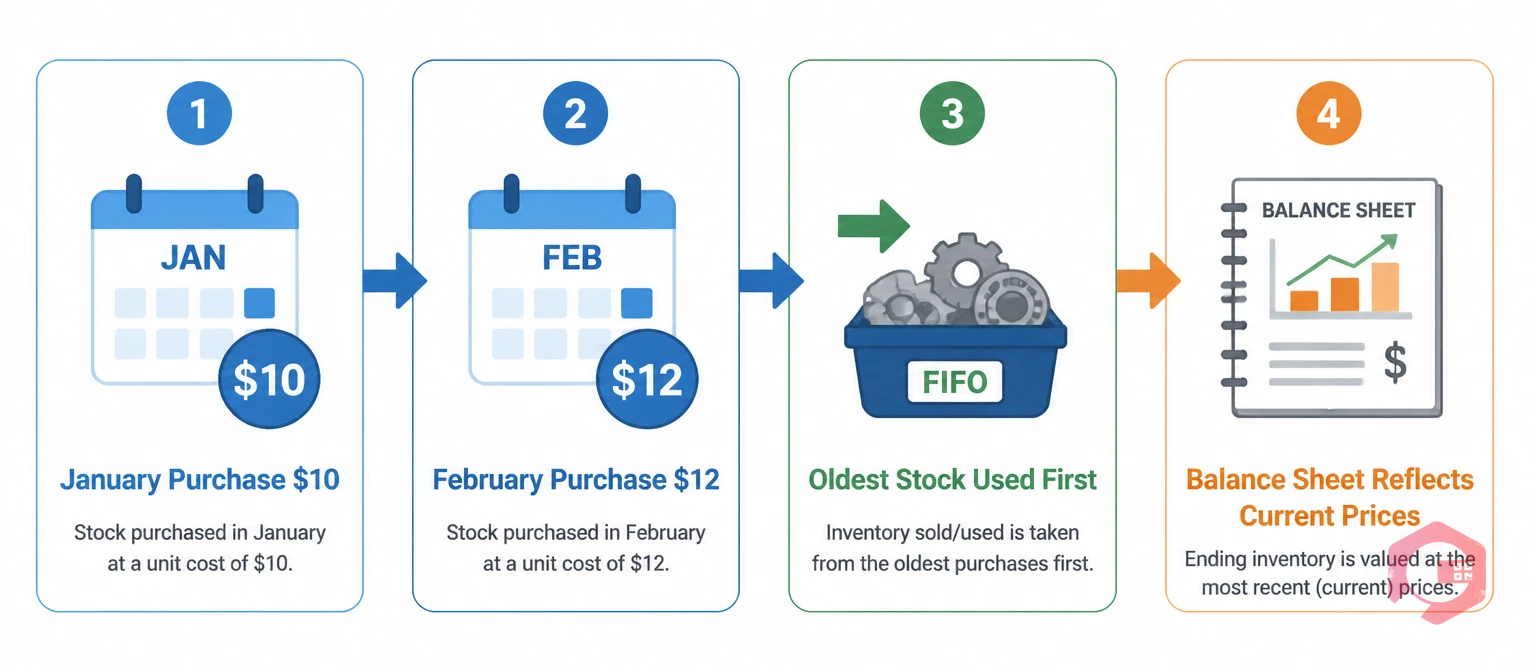

FIFO — First In, First Out — assumes that the earliest items purchased or produced are the first ones consumed or sold. Think of a stack of bearing replacements on a shelf: under FIFO, the oldest bearing (the one you bought first) goes into a work order before the newer ones.

Imagine your maintenance store receives three shipments of hydraulic filters:

If you use 150 filters in April, FIFO says the cost of those 150 filters is: 100 × $10 + 50 × $12 = $1,600. The remaining inventory carries the newer, higher-cost values — which means your balance sheet reflects closer-to-current prices.

FIFO matches the natural flow of most physical inventory. Older spare parts degrade over time, and using them first reduces the risk of expiry or obsolescence. It also produces a more realistic asset value on the balance sheet because remaining stock is priced at current or near-current costs.

LIFO — Last In, First Out — assumes the most recently acquired items are used first. Under LIFO, when you pull parts for a work order, you're drawing from the newest (and typically most expensive) stock first.

Using the same hydraulic filter example:

If you use 150 filters in April under LIFO, the cost is: 100 × $14 + 50 × $12 = $2,000. The remaining inventory is valued at older, lower prices — which understates the true current value of your stock.

LIFO is a tax strategy as much as an accounting method. When prices are rising, LIFO pushes higher-cost items into COGS first, reducing taxable income. US companies operating under GAAP sometimes use LIFO specifically for this reason — especially in inflationary periods.

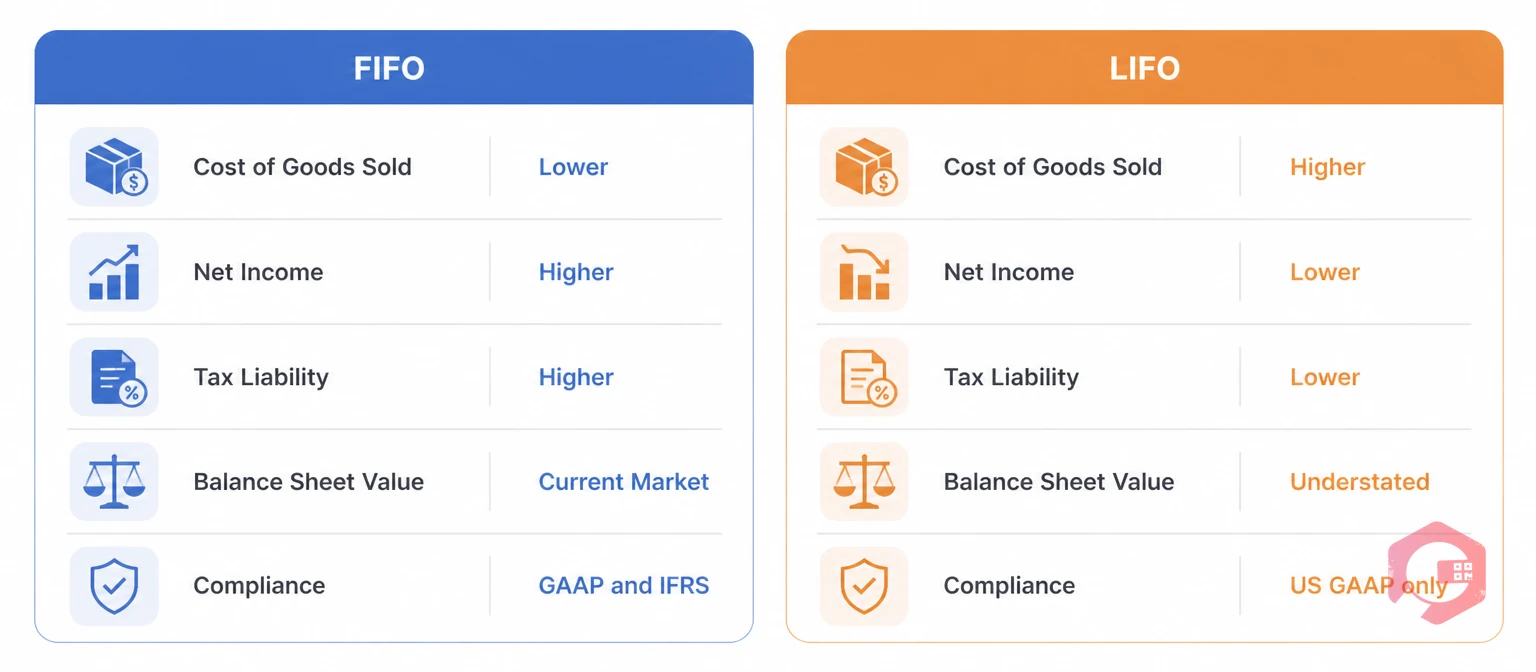

Here is how the two methods compare across the dimensions that matter most to maintenance and operations managers:

For most maintenance teams, inventory valuation feels like a finance department problem. It is not. The method your organization uses affects every part of your stores management — from how you justify capital spend to how you price out planned maintenance jobs.

When a technician pulls bearings, belts, or filters from the storeroom for a work order, the system needs to assign a cost to those materials. The valuation method determines that cost. Under FIFO, a filter pulled in Q4 might carry Q1's price. Under LIFO, it carries the most recent purchase price. This affects your cost-per-work-order reports, maintenance KPIs, and budget variance analysis.

FIFO naturally protects against obsolescence. Old parts consumed before new ones means your storeroom doesn't accumulate dead stock at stale prices. LIFO creates the opposite risk: older items sit at the bottom of the pile, potentially expiring or becoming unusable while carrying outdated cost values on your books. For maintenance inventory management, FIFO is almost always the safer operational choice.

Supply chain volatility since 2020 has made MRO pricing unpredictable. According to the ISM Report on Business, manufacturing supply prices saw sustained inflation for several consecutive years. In that environment, LIFO-using US facilities can show materially lower taxable profit — which frees up cash for capital reinvestment. However, finance teams must model the long-term "LIFO reserve" (the difference between FIFO and LIFO inventory values) to understand the full picture.

The financial consequences of choosing FIFO vs. LIFO go well beyond your storeroom. They ripple through your income statement, balance sheet, and tax filings.

Under FIFO during periods of rising costs, older (cheaper) stock flows through COGS first. That means:

Under LIFO in rising-price periods, newer (more expensive) items flow through COGS first. That means:

Companies using LIFO must track and disclose the "LIFO reserve" — the cumulative gap between LIFO and FIFO inventory values. According to FASB accounting standards, this disclosure is mandatory. The reserve grows over time in inflationary periods, and if a company switches from LIFO to FIFO, the entire reserve becomes taxable in the year of transition — a significant financial event.

There is no universal answer, but there are clear decision factors.

Many facilities use neither FIFO nor LIFO — they use the weighted average cost method, which smooths out price fluctuations by averaging the cost of all units on hand. This is the approach Cryotos CMMS supports alongside FIFO and LIFO. For maintenance stores with high transaction volume and many small-value parts, weighted average often provides the most stable and least administratively intensive result. See the inventory valuation glossary entry for a full breakdown of all three methods.

Manually tracking FIFO or LIFO layers across hundreds of SKUs is error-prone and time-consuming. Cryotos CMMS handles this automatically through its inventory management module, which supports Average Cost, LIFO, and FIFO valuation natively.

One manufacturing facility using Cryotos reduced inventory discrepancies by 40% within six months of switching from manual spreadsheet tracking to automated FIFO valuation — because the system enforced cost layer discipline on every transaction, not just at month-end close.

No. LIFO is explicitly prohibited under International Financial Reporting Standards (IFRS) as defined in IAS 2. Any company that files financial statements under IFRS — which includes most non-US public companies — must use either FIFO or the weighted average cost method. US companies filing under GAAP may use LIFO, but must disclose their LIFO reserve.

In an inflationary environment, yes — FIFO produces lower COGS, which means higher reported profit and higher tax liability compared to LIFO. However, when prices are falling (deflation), the relationship reverses: FIFO produces higher COGS and lower profit than LIFO. Most modern economies trend inflationary over time, so the tax advantage of LIFO is a real but context-dependent benefit.

Yes, but it requires IRS approval in the US and triggers a tax event. When switching from LIFO to FIFO, the entire accumulated LIFO reserve becomes taxable income in the year of the change. The IRS typically allows companies to spread this tax liability over four years. The decision should involve both your tax advisor and your CFO before any change is made.

The LIFO reserve is the cumulative difference between the inventory value under LIFO and what that same inventory would be worth under FIFO. It grows during inflationary periods and represents a deferred tax liability. Analysts often add back the LIFO reserve when comparing companies that use different valuation methods, to normalize their balance sheets for apples-to-apples comparison.

FIFO is the most practical choice for most maintenance spare parts operations. It matches the physical reality of how parts should be used (oldest first to prevent expiry), it is accepted globally under both GAAP and IFRS, and it produces a balance sheet that accurately reflects current inventory value. CMMS systems like Cryotos can enforce FIFO automatically, eliminating the manual effort of tracking cost layers in a spreadsheet.

FIFO and LIFO are not just accounting technicalities — they shape how your maintenance costs are reported, how your inventory is valued on the balance sheet, and how much tax your facility pays. FIFO is the simpler, globally accepted method that aligns with physical stock rotation. LIFO offers a tax deferral advantage for US companies during inflationary periods, but comes with significant complexity and global restrictions.

For most maintenance and operations teams, the right answer is FIFO — especially if you manage perishable parts, operate internationally, or want an accurate real-time picture of your inventory value. If you're ready to automate your inventory control and eliminate manual cost-layer tracking, Cryotos CMMS can configure your preferred valuation method from day one. Book a free demo today to see how it works in practice.

Cryotos AI predicts failures, automates work orders, and simplifies maintenance—before problems slow you down.