FIFO (First In, First Out) and LIFO (Last In, First Out) are the two primary inventory valuation methods used to calculate the cost of goods sold and ending inventory value. Under FIFO, the oldest stock is assumed to be sold first; under LIFO, the most recently acquired stock is sold first. The method you choose directly affects your gross profit, tax liability, and balance sheet — making it one of the most consequential decisions in inventory accounting. According to the IRS Publication 538, LIFO requires a special election and is prohibited under IFRS, which affects companies operating in GCC and Indian markets.

Key Takeaways

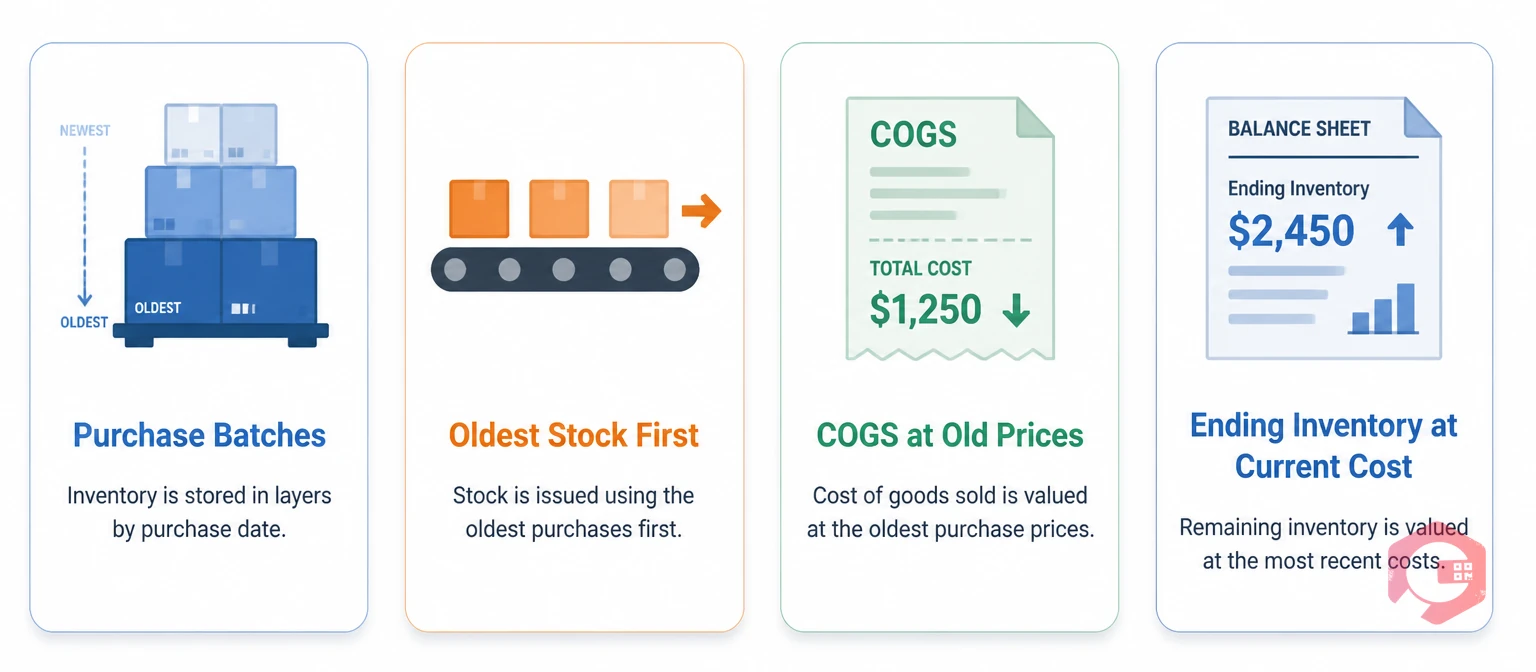

FIFO stands for First In, First Out. It assumes that the earliest purchased or manufactured inventory items are the first to be sold or used. This means the cost of goods sold reflects the oldest purchase prices, while ending inventory on the balance sheet reflects the most recent (and typically higher) prices.

FIFO is the most widely used inventory valuation method globally and is accepted under both US GAAP and IFRS. It's the default approach for companies in India, UAE, Saudi Arabia, and other GCC markets where IFRS governs financial reporting.

Each time you consume inventory, the system matches the usage against the oldest open purchase order first. Once that batch is exhausted, the next oldest batch applies. The remaining inventory on hand carries the cost of the most recently received batches.

Cryotos inventory management supports FIFO natively, automatically consuming stock from the oldest received batch during each work order issue.

Assume a maintenance team purchases lubricant oil in three batches:

If the team uses 150 litres in April, FIFO assigns: 100 litres x ₹50 + 50 litres x ₹55 = ₹7,750 as the cost of goods used. The remaining ending inventory is 50 litres x ₹55 + 100 litres x ₹60 = ₹8,750.

LIFO stands for Last In, First Out. It assumes the most recently purchased inventory is the first to be consumed or sold. This means the cost of goods sold reflects the latest (and typically highest) purchase prices, while ending inventory carries older, lower-cost layers.

LIFO is permitted only under US GAAP. It is explicitly prohibited under IAS 2 (IFRS), which means companies in India, GCC countries, and most of the world outside the US cannot use it for statutory financial reporting.

Each consumption transaction is matched against the most recently received cost layer. Older purchase layers sit in ending inventory, often understating the true current value of stock on hand.

Using the same three lubricant oil batches from the FIFO example above, LIFO assigns the 150-litre usage as: 100 litres x ₹60 (Batch 3) + 50 litres x ₹55 (Batch 2) = ₹8,750 as the cost of goods used. The remaining ending inventory is 50 litres x ₹55 + 100 litres x ₹50 = ₹7,750 - a lower balance sheet value than FIFO.

The table below covers every major dimension where FIFO and LIFO diverge - from accounting treatment to operational suitability.

| Attribute | FIFO | LIFO |

|---|---|---|

| Assumption | Oldest stock sold first | Newest stock sold first |

| COGS (rising prices) | Lower - older, cheaper costs | Higher - recent, costlier prices |

| Ending inventory value | Higher - reflects current prices | Lower - reflects older prices |

| Net income (rising prices) | Higher reported profit | Lower reported profit |

| Tax impact (US, rising prices) | Higher tax liability | Lower tax liability |

| Accounting standard compliance | GAAP and IFRS | US GAAP only (banned under IFRS) |

| Best for perishables / time-sensitive stock | Yes - matches physical flow | No - creates obsolescence risk |

| Balance sheet accuracy | High - inventory at current cost | Low - inventory may be understated |

| GCC / India suitability | Required (IFRS mandatory) | Not permitted |

| Inventory complexity | Moderate - oldest layers first | Higher - LIFO reserve tracking needed |

For most manufacturing and maintenance operations outside the US, FIFO is not just preferred - it's the only legally compliant method.

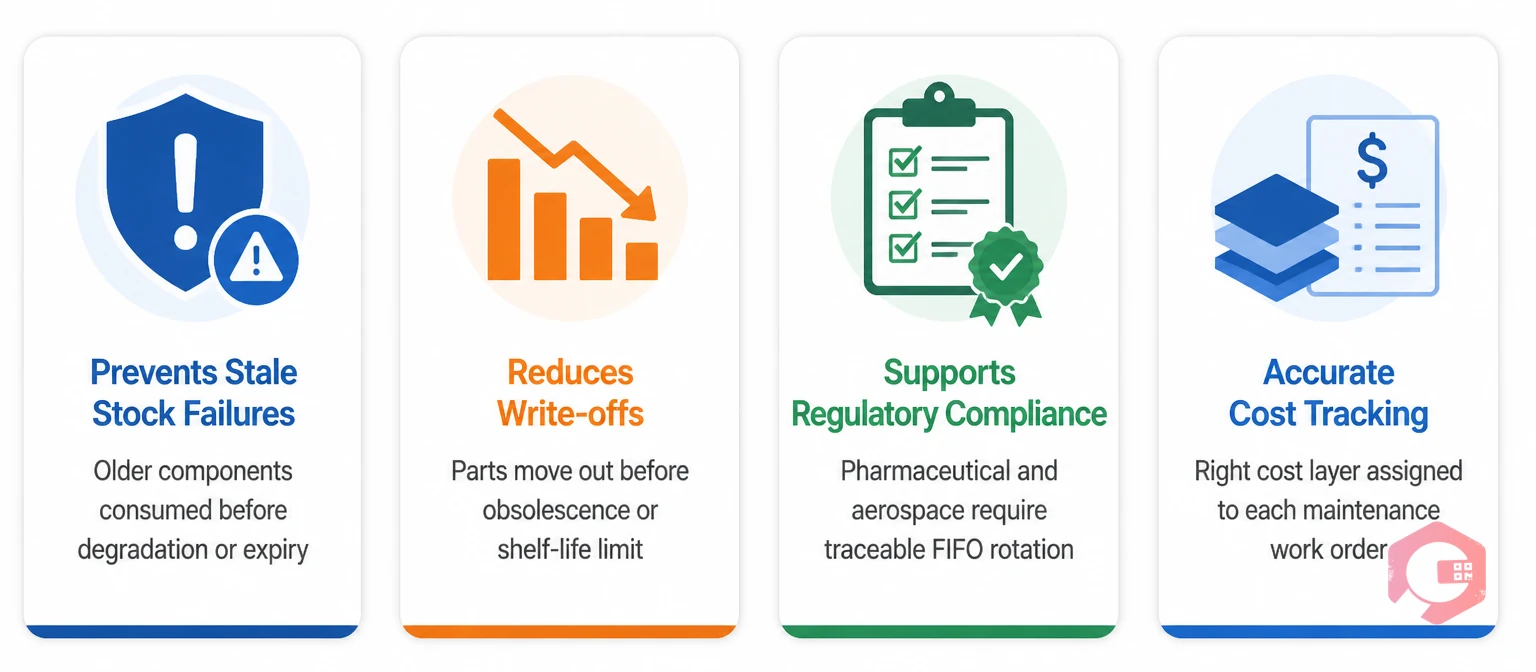

Most FIFO vs LIFO discussions focus on retail or manufacturing finished goods. But for maintenance teams managing MRO (Maintenance, Repair, and Operations) spare parts, the choice has direct operational consequences beyond accounting.

Spare parts have shelf lives, calibration expiry dates, and degradation risks. A bearing that was received 18 months ago may have developed micro-corrosion even if it was stored properly. Under LIFO, the most recently received bearings get issued first - the older stock stays in the warehouse indefinitely.

This is why FIFO is the operationally correct default for MRO inventory:

Use the MRO inventory checklist to audit whether your current stock rotation aligns with your FIFO policy.

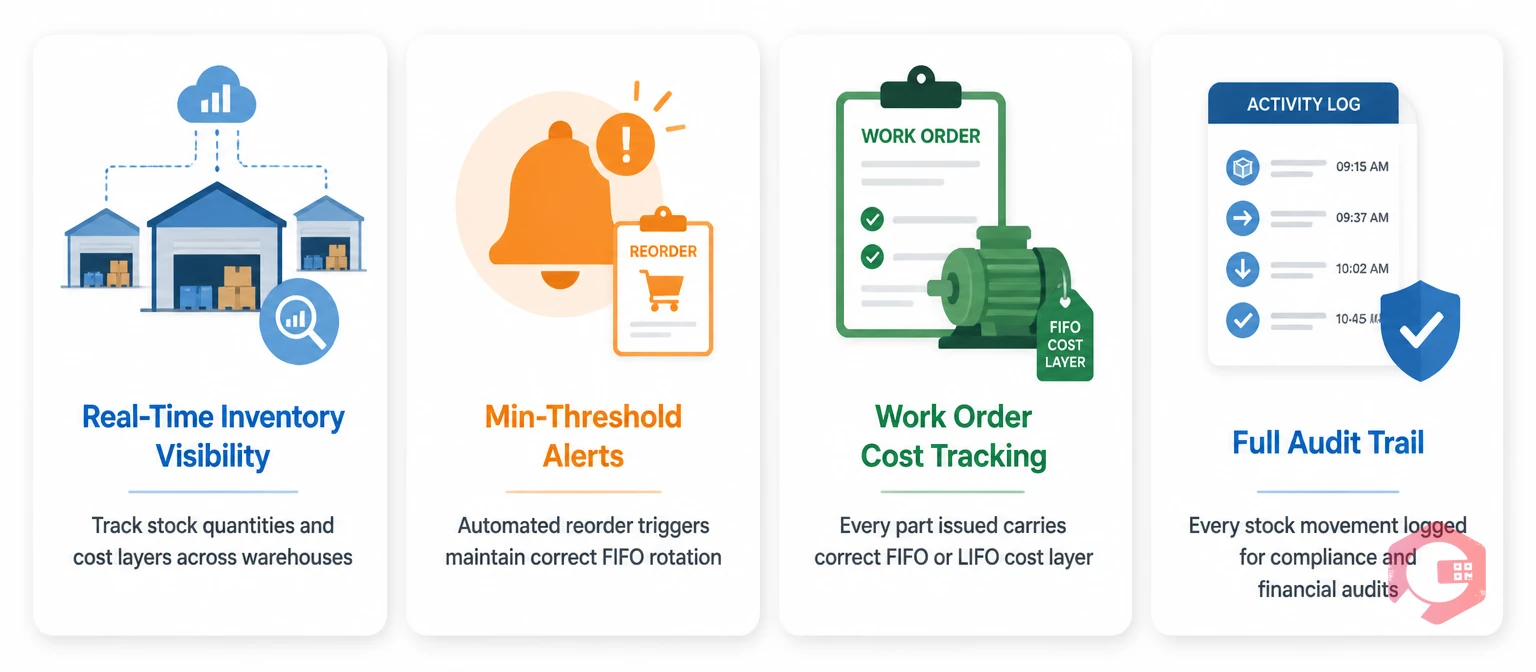

Cryotos spare parts inventory software enforces FIFO automatically at the warehouse level - so technicians always pull from the correct cost layer without manual tracking, and your warehouse management stays aligned with your costing policy.

The tax impact of FIFO vs LIFO is most significant during inflationary periods, when purchase prices are rising consistently. The method you choose can meaningfully shift your taxable income - particularly relevant for manufacturing and distribution businesses with high inventory turnover.

Under FIFO, COGS reflects older, lower prices. This produces a higher gross profit and higher taxable income. For US companies, this translates to a larger tax bill in inflationary periods. However, the balance sheet shows inventory at closer to current replacement cost, which improves perceived solvency and access to credit.

Under LIFO, COGS reflects the most recent (higher) prices, reducing gross profit and taxable income. This is the primary reason US companies elect LIFO - it defers tax payments during inflation. However, the FASB ASC 330 requires companies using LIFO to disclose their LIFO reserve - the difference between what inventory would have been worth under FIFO and what it's recorded at under LIFO.

For companies in India and GCC countries, this entire debate is moot: IFRS prohibits LIFO outright, so tax planning must work within FIFO or weighted average cost frameworks.

The right method depends on your geography, industry, and accounting priorities. Use this decision matrix as your starting point.

| If You Are... | Use This Method | Reason |

|---|---|---|

| Operating under IFRS (India, GCC, EU, etc.) | FIFO or Weighted Average | LIFO is prohibited by IAS 2 |

| US-based, inflation is high, minimising tax is priority | LIFO | Higher COGS reduces taxable income |

| Managing perishable or time-sensitive inventory | FIFO | Matches physical rotation, prevents spoilage |

| Manufacturing / MRO spare parts | FIFO | Prevents stale stock failures; operationally correct |

| Seeking accurate balance sheet / investor reporting | FIFO | Inventory reflects current replacement cost |

| High inventory with stable pricing | Weighted Average Cost | Smooths price fluctuations; simpler to manage |

If you're a maintenance or facility management team in India or the GCC, FIFO is both the compliant and operationally correct choice. For US-based manufacturers weighing tax optimisation, LIFO may offer short-term advantages - but at the cost of balance sheet transparency.

Manually tracking cost layers for hundreds of spare part SKUs is error-prone and time-consuming. A CMMS eliminates that burden by enforcing your chosen valuation method automatically at the point of issue.

Cryotos supports FIFO, LIFO, and Average Cost methods natively. When a technician scans a QR code to issue a part against a work order, the system automatically assigns the correct cost layer - no manual calculation needed. This keeps your maintenance costs accurately tied to individual assets and work orders.

The BI dashboard and report builder let you slice inventory costs by asset, location, or period - making it straightforward to reconcile physical stock movement with your financial statements. For teams that rely on SMRP best practices for maintenance planning, automated inventory costing is a foundational capability.

For most manufacturing companies - especially those in India, GCC, or any IFRS jurisdiction - FIFO is both required and operationally superior. It aligns with physical stock rotation, prevents stale component failures, and produces a more accurate balance sheet. US manufacturers may consider LIFO for tax deferral, but at the cost of balance sheet realism.

IFRS prohibits LIFO under IAS 2 because it does not reliably represent the physical flow of inventory and tends to understate ending inventory value during inflationary periods. IFRS prioritises faithful representation of financial position, making FIFO or weighted average the only permitted methods.

Yes, but it requires a formal accounting policy change, restatement of prior-period financials, and - in the US - approval from the IRS if LIFO was previously elected for tax purposes. The switch is treated as a change in accounting principle and must be disclosed in financial statements.

The LIFO reserve is the difference between the inventory value reported under LIFO and what it would have been under FIFO. It's a required disclosure for US GAAP companies using LIFO, and it helps analysts compare LIFO-using companies to those using FIFO on an apples-to-apples basis.

FIFO is the best method for MRO spare parts. Spare parts have shelf lives and can degrade in storage. FIFO ensures older stock is consumed first, reducing the risk of using degraded components and minimising write-offs. Most CMMS platforms, including Cryotos, enforce FIFO as the default for this reason.

Inventory valuation methods don't change actual cash paid for purchases, but they do affect taxable income - which changes how much cash goes to taxes. LIFO produces higher COGS in inflationary periods, reducing taxable income and preserving cash in the short term for US companies. FIFO has the opposite effect.

Poor inventory valuation practices cost maintenance teams more than just tax efficiency - they lead to stale stock, inaccurate asset costs, and compliance failures. Schedule a free demo to see how Cryotos automates FIFO, LIFO, and average cost inventory valuation across your maintenance operations.

Cryotos AI predicts failures, automates work orders, and simplifies maintenance—before problems slow you down.